As a first home owner, which loans are best for me?

The best home loan for any borrower is one that you can afford, with manageable repayments that will not leave you financially stressed each month.

As a first home buyer, looking through all the mortgages on offer can be daunting. In fact, the whole process can be very emotional. Initial excitement can quickly turn to confusion, then anxiety, overwhelm, and even confusion. But don’t worry, we are here to help.

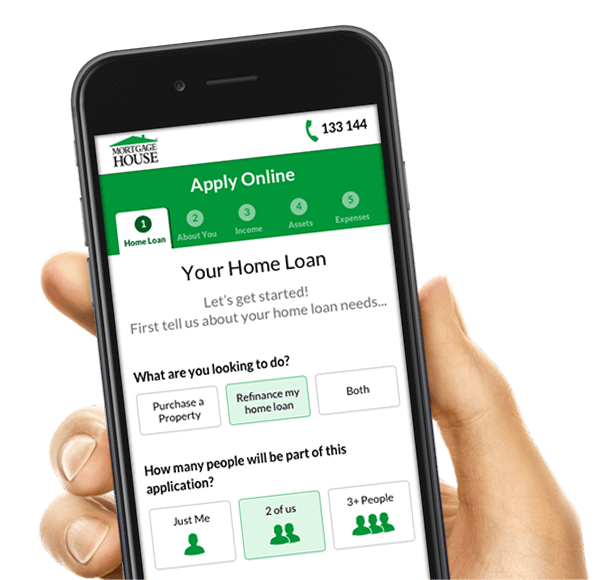

We can help you get to know the terminology surrounding mortgages and how to make all the calculations. At Mortgage House we understand being a first home owner means you probably won’t understand all the steps required to make your dream come true. We can walk you through these steps, starting with working out how much you can borrow, and what that means for weekly or monthly payments. Once you have that information, you can start looking for the house you have always wanted, with clear understanding of the first buyer loan products available from Mortgage House. We will guide you through the offer and purchase stages to ensure you feel that you are getting the best loan underpinned by the best support from our specialists.

Are home loans complicated?

The actual concept of a home loan is simple. It is all the steps involved with navigating the best home loan for your needs that can get complicated for a first home buyer. That’s where we come in. As one of Australia’s largest independently owned non-bank lenders, we understand the mindset of first home buyers and can easily guide you through the process. We have access to a range of first-time buyer home loans that can specifically suit your needs as you enter the property market for the first time.

Finding the best one can be tricky, so being able to compare up to five at a time, using our experience, award-winning home loan comparison model, and the same resources as traditional brokers, will be a reassuring way to start. Our main goal is to help you find the lowest rate loan options to match your circumstances and guide you through the process seamlessly. If you have found your dream first home, we want to help you secure it and start your new life as soon as possible. Choose an uncomplicated experience with our support, tools, knowledge and experience to find great comparison deals quickly.

How does the first home owner grant work?

Since the dawn of this century, being an Australian first home buyer has meant having access to a first home owner grant. They started as an offset to the GST and have been used as a mechanism by most Australian States and Territories to stimulate the economy, create jobs and make mortgages more affordable for the first home buyer. They usually take the form of a one-off grant to those who are eligible.

Income and age aren’t usually a factor, and States will often put a cap on the price of the house to ensure those who really need it have access to it. Some States might also make the grants higher for first home buyer mortgages in regional areas, or for new homes only.

In most States, you will need to live in the house for a minimum of six months, and it must be your primary place of residence. To find out whether or not you are eligible, or to work out exactly how the first home owner grants work in your State, contact us, or visit www.firsthome.gov.au

What are my home loan options?

There are four main kinds of loans that can be available to the first home buyer. Knowing how each of them works can be more than just handy, it can save you money, now and in the future. The first one is the variable rate home loan. This can be a good way to leave some money in your pocket, and even give you the chance to pay it off sooner if you want to. The rate referred to is the interest rate, which will usually be lower than a fixed rate loan.

As a first home buyer, having a variable rate loan means you can pay more off if you want, without penalties, but it also means the rate may change, either up or down. That can make things hard when it comes to budgeting. With a fixed rate loan, you can fix the interest rate for between one and five years, and renegotiate after that if you want. These mortgages can make it easy for budgeting, as you know exactly how much your repayments will be each time they are due.

If interest rates rise, yours won’t, however some fixed rates can be higher than variable rates. Some of our fixed rate loans allow you to make extra payments if you wish. Having the same access to mortgages as the large lenders also means you can split your loan into periods of fixed and variable interest rates, if you want to, subject to a few conditions. And finally, construction loans give you the flexibility to draw down your loan as it is being built. Feel free to get in touch with a first home buyer specialist at Mortgage House to provide advice about the best home loan option for you, based on your exact circumstances.

What is Stamp Duty?

When you are a first home buyer, the reality of having to pay stamp duty can be a real pain. Stamp duty in Australia is often different in each State. It is basically a tax the State charges on the sale value. It is calculated on the higher of either the purchase price or the current market value. The cost of it can be quite high, and it can often come as a surprise to a first home owner. Use our stamp duty calculator to help limit your surprise. Our Mortgage Specialists can provide you with relevant Stamp Duty Calculations so you can stay informed.